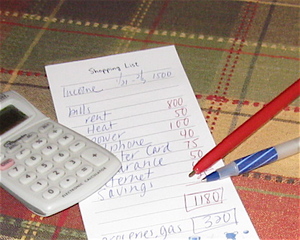

Home budgeting is the process of tracking our income and expenses. For those of us with a limited income, budgeting is the plan we’ve cooked up for paying the bills while leaving enough left over for groceries, gas for the car and other little miscellaneous expenses that pop up every month.

While there are all sorts of budget software programs out there, one of the easiest ways to budget is what I call “refrigerator budgeting.” Refrigerator budgeting is scribbling down a simplified home budget on a scrap of paper, and then posting it on the frig where it can be seen. It works for me and should work for you as well. Here is how it’s done:

1. Determine your monthly income. Record all the income earned in a month on note paper. Record the income earned between the 1st-15th of the month in one column, and the 16th-31st in a second column.

2. Assemble your monthly bills & average food and fuel costs Bills are those normal monthly expenses that you are obligated to pay such as the rent or mortgage payment, utilities, insurance, car payment, internet fees, phone, credit cards, and medical bills. Also to include is an average monthly cost for groceries and fuel (you may have backtrack three months to determine a reasonable average).

Assign the bills to either one of the two columns, depending on when they fall due. Food & fuel should be split in half with an equal amount assigned to each column.

-75

Insurance

-50

Internet

-40

Savings

-25

Food

-350

Fuel

-100

16th-31st of month

Income

$1500

Car loan

-300

Macys

-50

Medical

-100

Savings

-75

Food

-350

Fuel

-100

4. Subtract the bills. Subtract your financial obligations for each two week cycle from the income earned in that week. Using our example, bills for the first half of the month totaled $1630, and $975 for the second part of the month, leaving only $395 a month for this family to spend on incidentals.

5. Making sense of the numbers. With your family’s financial picture now written in black and white, it becomes much easier to isolate the problems in your budget and figure up a strategy for staying out of financial trouble. Common problems to address include:

—Not having enough funds in the first half of the month to pay for groceries. This can be fixed by carrying over a few hundred dollars from the previous paycheck.

—Overspending . If you spend $600 a month in incidentals when all you’ve got is $395 to work with, you’re overspending. One easy strategy is to cash out $395 a month from your paycheck to fund incidental costs. When that money is gone, the spending stops too.

—Not enough going to debt reduction. Minimum payments on charge cards means that you could be making payments clear into 2020. To pay down credit debt, trim back the grocery bill and double your credit card payments.

—Too little to savings. Ideally, your emergency fund should contain 3-6 months of living expenses. As long as you are still paying down debt, limit your emergency fund to $1000. When the debt is gone, you can then accelerate the savings.

6. Post these numbers on the refrigerator. Once your household budget has been drawn up, post it on the frig as a daily reminder of your financial goals. Keeping your goals in the forefront of your mind is what will keep you on the right track to financial independence.

For more budget related articles by this contributor:

5 top personal financial planning tools.

How to pay off credit card debt in a tough economy.

How to save money without changing your lifestyle.