Remember Popeye’s old friend J. Wellington Wimpy who would “Gladly pay you Tuesday for a hamburger today”? Similarly, the IRS will gladly tax you today for interest you may receive at some point in the future and call it OID (Original Issue Discount) interest.

Many investors who receive a 1099-OID for tax reporting are completely bewildered as to exactly what it represents. With a shrug of their shoulders they report OID on their tax returns as interest and promptly forget about it. However, it’s very important to at least have a conceptual understanding of what OID represents. It’s one area where erroneous treatment can result in thousands of dollars of unnecessary tax overpayments.

OID is intended to be an annual recognition of estimated amortized interest resulting from buying a debt instrument such as a bond or CD at a discount. Typical securities that generate OID include federal strips, collateralized debt obligations and zero coupon corporates, certificates of deposit, municipals, Eurobonds and government agency bonds.

OID is not always reported accurately and is almost always wrong when the security is purchased in the secondary market instead of at initial issue. Unless you enjoy receiving computer generated correspondence from the Internal Revenue Service you’ll have to report the figures provided to you by the brokerage firm or reporting entity on your tax return. This is what most people do but it is very easy to forget about the OID that was reported in the past in the year the security matures or is sold.

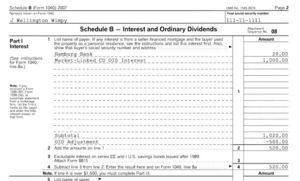

Consider the case of the market-linked CD. These are zero coupon, principal protected instruments that pay interest at maturity based upon the performance of an underlying index such as the S&P; 500, Dow Jones Eurostoxx 50, commodity indexes/prices or even foreign currency movements relative to the dollar. There is no interest paid until maturity. Holders of these securities receive annual 1099-OID reporting even though it’s unknown whether or not there will be any interest paid at maturity. For example, an eight year S&P; 500 linked CD bought in March of 2000 for $20,000 when the index was at 1500 returned $20,000 in March of 2008 with the S&P; 500 at 1300. The full amount of the original investment was returned despite the 13% drop in the index because of the underlying principal guarantee. In this example, eight years of OID was reported to the owner of this CD and has been reported as interest on the tax return. Using a simplifying assumption of a 5% rate per year this will amount to over $8,000 of OID interest that was reported but never received.

In this market-linked CD example an $8,000 OID adjustment is required to properly recognize the fact that no profit or loss was recognized on this investment. The adjustment is shown as a negative number on Schedule B of the tax return. An easy way to keep track of the data is to create a spreadsheet that tracks the OID being reported each year by the individual securities that generate OID.

A way to avoid OID reporting and the necessity to track it over time is to buy these types of securities only in IRAs or retirement plans. It’s noteworthy that some of the most suitable investments for retirement accounts, where principal protection is of significant value, generate 1099 OID reporting in taxable accounts.

Registered Representative of and Securities offered through Financial West Group (FWG), Member FINRA/SIPC